On July 14, 2026, IBM shares fell about 25 percent in a single day. That is the worst day in the company’s 115-year history, worse even than Black Monday in 1987. Roughly 67 billion dollars of market value disappeared before the closing bell. The company had preannounced a bad quarter, with revenue around 17.2 billion against the 17.86 billion Wall Street expected.

Plenty of the coverage put the mainframe at the center of it. And I understand why. I have spent close to twenty years working on these systems and sometimes migrating them, so anything with the word mainframe in it lands on my desk. But if you read the story as “people are finally walking away from the mainframe,” you are reading it wrong. That is not what happened.

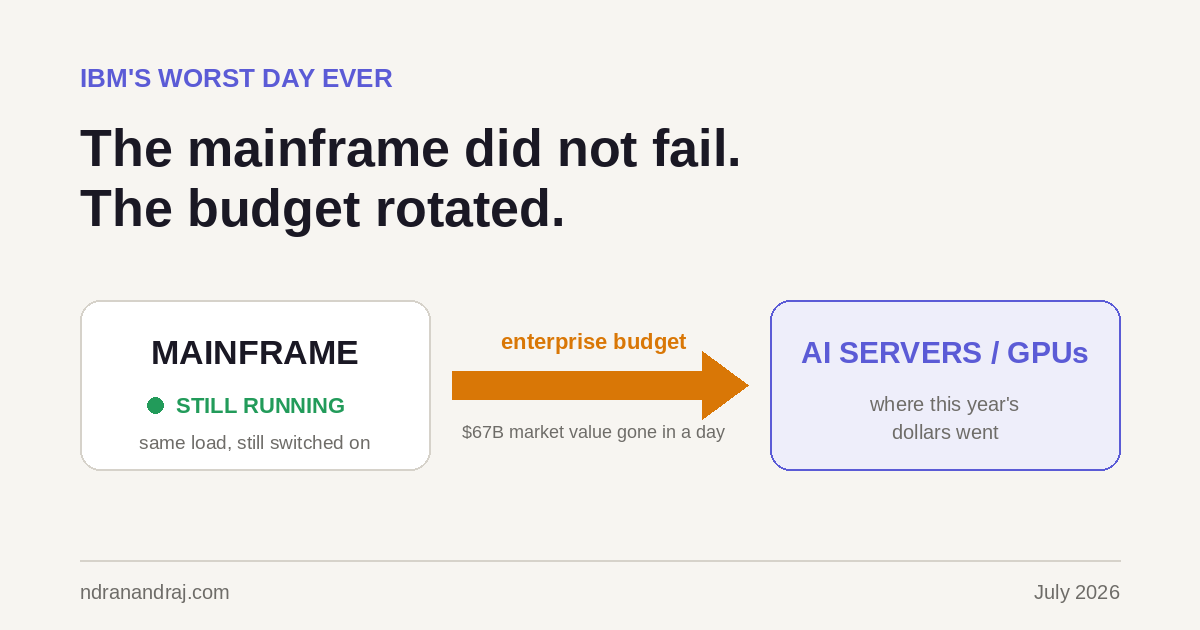

What actually dropped

IBM’s infrastructure division, the part that includes the mainframe, fell about 7 percent. The CEO, Arvind Krishna, said they had planned for a low single digit decline in the z17 mainframe line. Instead it came in much worse. Two things drove that gap, and neither of them is customers deciding the mainframe is dead.

The first is a global memory shortage. Chip costs went up, and a machine as memory heavy as a mainframe feels that directly. That is a supply problem, not a demand problem.

The second is more interesting, and it is the actual headline. Money is rotating. Enterprise budgets are shifting out of traditional infrastructure and software and into AI servers and memory. The same customers are still there. They are just spending this year’s dollars on GPUs instead of on the next hardware refresh. The mainframe did not lose an argument. It lost a budget cycle.

The same filter, again

I wrote earlier this year about a filter I use for every “this changes everything” claim in my field. The hype is always about replacement. The reality is almost always about layering. A new technology rarely kills the core. It becomes a layer next to it.

This week fits that filter cleanly. Nobody switched off a mainframe to buy an AI server. The core is still running the same banking and insurance and airline transactions it ran last month. What changed is that the growth money went somewhere shinier for a quarter. That is a spending shift, not a replacement. If you had bet on the funeral, you would have called this wrong.

That distinction matters if you work anywhere near these systems. A budget can rotate back. A memory shortage eases. A replaced system does not come back. Reading a bad quarter as the end of the mainframe would lead you to exactly the wrong decisions about where to put your career and your team’s time.

One honest caveat

These were preannounced numbers. IBM reports full second quarter earnings on July 22, so there is more detail coming, and some of what I have described may sharpen or shift when the real report lands. I am also not here to tell you whether the stock is cheap now. That is not my lane, and anyone who says they know is guessing.

What I will say is this. When a 115-year-old company has its worst day ever and the easy story is “the old thing is finally dying,” that is exactly the moment to slow down and check whether anything actually died. This time, nothing did. The money just moved.